From 2009 to 2020, the global autonomous car market evolved from experimental projects to a multi-billion dollar industry.

During these years, key trends shaping the economics of self-driving transport emerged:

- Some companies (Aurora Innovation, Arrival) went public. The projects with strong corporate backing, Waymo (a division of Google) and Cruise (the autonomous vehicle division of General Motors), achieved the highest market valuations during this period.

- Former employees of pioneering companies began founding their own startups

- Large corporations rapidly acquired AVs companies and created specialized divisions

- Billions of dollars in investment poured into the industry at an unprecedented rate

Financing AV Projects: Four Sources of Capital

By 2020, autonomous vehicles were just beginning their journey toward mass commercialization. Companies were offering autonomous transportation services in only a few locations: San Francisco, Beijing, and Shanghai. Significant investments were required to develop the technology, expand fleets, and hire specialists.

We identified four main funding methods for autonomous vehicle projects.

External investment

The most common method of raising funds is external investment rounds from venture capital funds and corporate investors. This route has been chosen primarily by companies from the US, China, and the UK.

| Company | Year | Investors | Investment size |

| Cruise | 2018 | SoftBank Vision Fund, Honda | $2,25 bn (SoftBank), $2,75 bn (Honda) |

| AutoX | 2021 | Alibaba | $100 M |

| Five AI | 2020 | Sistema VC, international investors | $41 M |

| Comma.ai | 2019 | Andreessen Horowitz | $3,1 M |

| Argo AI | 2017-2022 | Ford Motor Co., Volkswagen Group | $1 M (Ford), $2,6 M (Volkswagen) |

| Nuro | 2019 | SoftBank Group | $940 M |

| Arrival | 2020 | Winter Capital, BlackRock, UPS | €50 M (Winter Capital), $118 M (BlackRock), €10 M (UPS) |

| Waymo | 2021 | Various investors | $5,5 bn |

Examples of major investments:

- Cruise raised $2.25 billion from SoftBank Vision Fund and $2.75 billion from Honda in 2018.

- Waymo raised $5.5 billion in 2021.

- Pony.ai raised funds, bringing the company’s valuation to $8.5 billion by 2022.

- WeRide raised $310 million from Alliance Ventures, the China Structural Reform Fund, and other investors.

Investments were often accompanied by strategic partnerships: investors received a stake in the company or the opportunity to integrate their technologies into the unmanned systems being developed.

Internal investment

Many corporations have funded their own drone divisions or subsidiaries:

- Yandex invested 1.5 billion rubles (approximately $24.2 million) in its self-driving division in 2019, and another 754 million rubles ($10.5 million) in the first quarter of 2020.

- Cognitive Technologies planned to invest 750 million rubles in the development of the C-Pilot autonomous driving system between 2016 and 2019.

- BaseTrack founder invested approximately $1 M in the company at the initial stage.

State and municipal grants

This source of funding was chosen primarily by European companies developing experimental products:

- Oxbotica received $10.5 million from Innovate UK in 2017.

- Five Al raised $16.6 million from the UK Department for Business and Transport in 2017.

- Arrival received $2 million from the US Federal Transport Administration in 2021.

Public funding usually comes with commitments to cities and local communities, such as job creation or local infrastructure development.

Commercial loans

Some companies have attracted bank financing. For example, BaseTrack received two loans from SME Bank totaling 88 million rubles (approximately $1.2 million) at a preferential rate of 7% per annum as part of a startup support program.

Valuation of AV companies

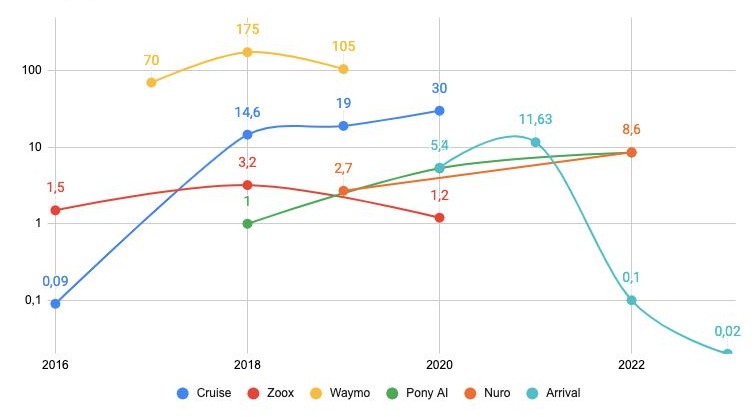

Robotaxis lead in ratings

Companies developing robotaxis were valued significantly higher by investors than manufacturers of other types of autonomous vehicles. This is due to the higher revenue potential and the revolutionary nature of the technology, which has the potential to radically change urban mobility.

Leading Company Valuation Trends:

- Nuro: Value increase to $8.6 bn in 2022

- Waymo: From $70 bn in 2017 to $175 bn in 2018, then declining to $105 bn in 2019

- Cruise: Rapid growth from $1 bn in 2017 to $30 bn in 2021

- Pony.ai: Valuation increase from $1 bn in 2018 to $8.5 bn in 2022

Reality vs. Expectations

Interestingly, the actual deal prices for autonomous vehicle companies often differed from their pre-money valuations:

Cruise was acquired by General Motors in 2016 for $1 billion, with a pre-money valuation of only $90 million.

Zoox was acquired by Amazon in 2020 for $1.2 billion, with a valuation of $3.2 billion.

These discrepancies reflect changing market expectations: while in 2016 investors were optimistic about the rapid adoption of autonomous technology, by 2020 it became clear that the mass adoption of autonomous vehicles was delayed.

The rise and fall of public companies

The fate of publicly traded self-driving companies has been particularly dramatic:

Arrival reached a market capitalization of $13 billion after its IPO, but by 2023, its value had fallen to $20 million.

Tesla, although not a pure self-driving company, reached a market capitalization of $555.24 billion in 2020, becoming the sixth-most valuable American company.

Financial results: profit or loss?

By the end of 2020, most self-driving car companies were unprofitable and were still actively investing in technology development.

Among the exceptions:

- Navya, a manufacturer of unmanned space shuttles, posted positive revenue: €10.28 million in 2017, growing to €19.012 million in 2018 (+85%).

- Tesla posted a profit of $331 million in the third quarter of 2020 (+131% compared to the same period in 2019).

Mergers and acquisitions: corporate consolidation

A wave of corporate acquisitions has changed the landscape of the self-driving industry:

- General Motors acquired Cruise for $1-1.2 billion in 2016.

- Hyundai Motor Group and Aptiv formed the joint venture Motional, valued at $4 billion in 2019.

- Amazon acquired Zoox for $1.2 billion in 2020.

- Aurora Innovation acquired Uber’s self-driving division (Uber ATG) at a $4 billion valuation in 2020.

- Toyota Woven Planet Holdings acquired Lyft’s self-driving division for $550 million in 2021.

These deals reflect the desire of large corporations to strengthen their position in a promising technology niche by gaining access to talented engineers and ready-made technological solutions.

Key findings

- High Investment Rates: Over $30 billion was invested in autonomous driving technologies between 2009 and 2020, reflecting high investor expectations.

- Corporate Support as a Key Factor: Projects with the backing of large corporations (Google’s Waymo, GM’s Cruise), which were able to fund long-term research, proved the most sustainable.

- Uneven Value Distribution: Robotaxi developers received the highest valuations, significantly outpacing the makers of autonomous shuttles and personal vehicles.

- Adjustment to Expectations: Toward the end of the period under review, the market began to adjust its inflated expectations regarding the timeline for mass adoption of autonomous driving technologies, which resulted in lower valuations for some companies.

- Delayed Profitability: With the exception of a few companies, most projects have not demonstrated profitability, continuing to require significant investment in research and development.

The autonomous vehicle economy continues to emerge, transforming the market structure: technology leaders are emerging, assets are being consolidated through mergers and acquisitions, and companies that fail to attract sufficient funding or fulfill their investor commitments are being forced to revise their strategies or exit the market. These processes reflect the industry’s evolution from an early experimental stage to a more mature phase of development with increased focus on operational efficiency and commercial viability.